Our investment philosophy strictly adheres to the following core principles:

- Risks and returns are interrelated

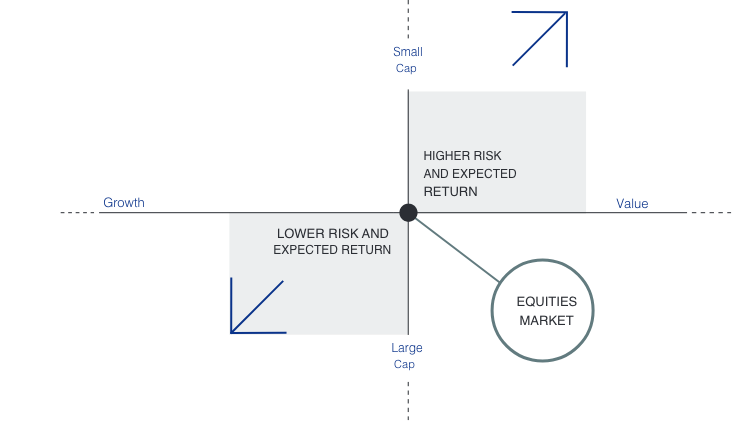

- Small caps have a higher expected return than large caps

- Cheaper value stocks have a higher expected return than more expensive growth stocks

|

The past teaches us that it is practically impossible achieving consistently higher returns on a long-term basis by market timing and stock picking. Nevertheless, market-timers and stock-pickers try to obtain an outperformance by foreseeing rising or falling share prices or by trying to identify under- or overvalued stocks. |

|

Percentage of European Equity Funds Outperformed by Benchmarks

| Fund Category | Comparison Index | One-Year | Three-Year | Five-Year | Ten-Year |

| Europe Equity | S&P Europe 350® | 74,79 | 62,22 | 72,63 | 83,23 |

| Eurozone Equity | S&P Eurozone BMI | 65,43 | 72,47 | 83,36 | 93,20 |

| France Equity | S&P France BMI | 83,33 | 71,69 | 93,18 | 92,86 |

| Germany Equity | S&P Germany BMI | 40,45 | 49,48 | 62,64 | 76,34 |

| Global Equity | S&P Global 1200 | 80,35 | 68,97 | 76,83 | 89,69 |

| Emerging Markets Equity | S&P/IFCI Composite | 66,19 | 59,24 | 70,35 | 86,11 |

| U.S. Equity | S&P 500 | 82,41 | 67,80 | 73,84 | 94,74 |

Source: S&P Dow Jones Indices LLC, Morningstar. Data for periods ending Dec. 31, 2021. Outperformance is based on equal-weighted fund counts.

Index performance based on total return. Past performance is no guarantee of future results. Table is provided for illustrative purposes.

Harry M. MARKOWITZ was awarded the Nobel Prize in Economic Sciences for his work on optimal diversification. He argued that much higher returns can be achieved by controlling risk.

To guarantee long-term asset growth, investors need to maintain an optimally diversified portfolio, according to MARKOWITZ’S theory.

|

|

Eugene F. FAMA, Nobel Prize in Economic Sciences 2013, from the University of Chicago Booth School of Business and Kenneth R. FRENCH from Dartmouth College observed that two types of stocks, small caps and value caps, tended to perform better than the market as a whole. Their research findings have provided a better understanding of the factors that drive asset management performance.

S & P 500 INDEX1928-2022 Data provided by |

|

dimensional us large cap value index1928-2022 Index data compiled by Dimensional. |

|

dimensional us small cap index1928-2022 Index data compiled by Dimensional. |

|

This figure shows the historical return advantage of small stocks over large and value stocks over growth. Small company stocks are riskier than large company stocks, and have therefore delivered a higher return. Value stocks have low prices relative to their underlying accounting measures such as book value, sales and earnings. Growth stocks have high stock prices relative to their underlying accounting measures. The size and value effects are strong around the world.

Historical returns around the world; Annual data; % per annum

Source: dimensional

Randomness of returns. No one knows which markets will outperform from year to year. By investing in a diversified portfolio you capture returns wherever they occur. Maintain a fixed asset allocation through rebalancing.

| Annual Returns in EUR | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| MSCI WORLD INDEX (NET DIV.) | Highest Return |

37% | 0% | 22% | 32% | 22% | 22% | 23% | 20% | -4% | 30% | 9% | 31% | 0% |

| MSCI EUROPE INDEX (NET DIV.) | 28% | -2% | 17% | 22% | 19% | 10% | 15% | 10% | -6% | 29% | 9% | 28% | -10% | |

| MSCI USA SMALL CAP INDEX (NET DIV.) | 25% | -8% | 16% | 22% | 13% | 8% | 11% | 10% | -6% | 26% | 6% | 25% | -11% | |

| MSCI JAPAN INDEX (NET DIV.) | 24% | -10% | 15% | 20% | 11% | 7% | 11% | 9% | -9% | 22% | 5% | 12% | -12% | |

| MSCI EMERGING MARKETS INDEX (NET DIV.) | 20% | -12% | 14% | 1% | 9% | 2% | 6% | 7% | -11% | 21% | -2% | 9% | -13% | |

| MSCI PACIFIC EX JAPAN INDEX (NET DIV.) | Lowest Return |

11% | -16% | 6% | -7% | 7% | -5% | 3% | 2% | -11% | 21% | -3% | 5% | -15% |

|

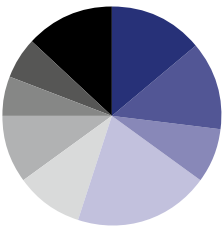

This example demonstrates the positive impact of optimal diversification on the fund’s performance and volatility. By investing 100% in Example 1, the annualised performance over the period is +4,18% with a volatility of 15,27%. Example 2, which is more diversified, offers a better return over the period, with no significant increase in volatility. Examples 3 and 4 show the same trend. Each time we increase the level of diversification, we note an improvement in returns. |

For our Enhanced Index Investing Equities sub-fund, we have taken this argument to its logical conclusion to achieve a maximum return, while maintaining a similar level of volatility to Example 1. The need for a well-diversified investment portfolio is a prudent principle and a key component of our investment philosophy. We aim to provide the best framework for your optimal asset allocation. |

| monthly : 01/1999-12/2022; in Euros | EXAMPLE 1 | EXAMPLE 2 | EXAMPLE 3 | EXAMPLE 4 | EXAMPLE 5 |

| MSCI EUROPE INDEX (NET DIV) | 100% | 50% | 40% | 30% | 13% |

| MSCI EUROPE EX UK INDEX (NET DIV) | 14% | ||||

| MSCI EUROPE SMALL CAP INDEX (NET DIV) | 6% | 10% | 8% | ||

| MSCI EUROPE VALUE INDEX (NET DIV) | 7% | 16% | 20% | ||

| MSCI EMERGING MARKETS INDEX (NET DIV) | 20% | 20% | 17% | 10% | |

| MSCI EMERGING MARKETS VALUE INDEX (NET DIV) | 10% | ||||

| MSCI PACIFIC SMALL CAP INDEX (NET DIV) | 6% | ||||

| MSCI USA SMALL CAP INDEX (NET DIV) | 3% | 6% | 6% | ||

| MSCI WORLD INDEX (NET DIV) | 30% | 24% | 21% | 13% | |

| TOTAL | 100% | 100% | 100% | 100% | 100% |

| ANNUALISED PERFORMANCE | 4,18% | 5,65% | 6,00% | 6,16% | 6,27% |

| ANNUALISED STANDARD DEVIATION | 15,27% | 15,05% | 15,33% | 15,54% | 15,52% |

|

|

|

|

|

Investors seeking greater expected return may increase their equity exposure while keeping liquidity and their bond portfolio short. Stocks offer an opportunity for higher long-term returns compared with bonds but come with greater risk. Bonds are generally more stable than stocks but have provided lower long-term returns.

For conservative investors, workers nearing retirement, and anyone looking to stabilize their portfolio during times of market volatility, the structure of their portfolio is the strategy.

Therefore, we created a bond fund based on two main factors. Term (Longer-term bonds are riskier and have higher expected returns than shorter-term bonds) and Credit (Lower credit quality bonds are riskier and have higher expected returns than higher credit quali

ty bonds). Our goal was to combine all this dimensions to reach the best risk/return profile.

By owning a mix of both funds, every investor can perfectly diversify his

portfolio in respect of his risk tolerance.

|

We created two sub-funds: an equity sub-fund, as it makes sense to invest a portion of a portfolio in asset classes with higher expected returns, and a bond sub-fund, to reduce the portfolio’s overall volatility. As an independent asset management company, Tareno (Luxembourg) S.A. will offer you the best possible advice to help you achieve an optimal balance between equities and bonds, while taking into consideration your risk tolerance, your liquidity needs and your investment horizon. |

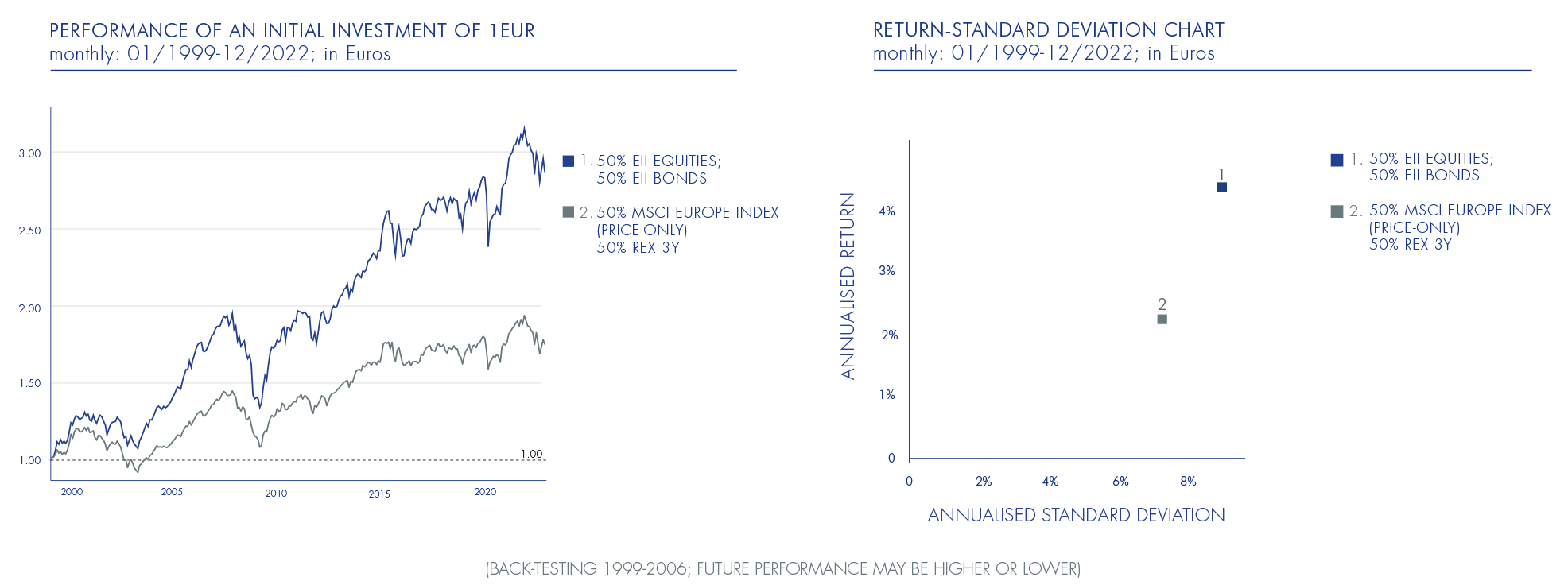

This is where index investing comes into its own, as it allows for considerable flexibility in the review process. Your advisor’s role is to ensure strict compliance with the asset allocation implemented and to closely monitor your risk spread over time. The example on the next page illustrates the relative performance of a diversified Tareno portfolio, invested 50% in equities and 50% in bonds, compared to its benchmark indices. (The REX 3Y index represents 3-year German Government Bonds) |